FAQs

Derivatives are financial contracts entered into today to agree to buy, sell, or have the right to buy or sell an “underlying asset” in the future. Simply put, the buyer and seller make an agreement today on the quantity and price of the underlying asset they will buy or sell, as well as when the delivery and payment will be made.

- The buyer and seller agree on a price today and make the delivery and payment in the future.

- The buyer is called a "long position."

- The seller is called a "short position."

- A derivatives contract has no value on its own. Its value depends on the asset or variable it is based on, which is called the "underlying asset."

Derivative products traded on the Thailand Futures Exchange (TFEX) are of two main types:

- Futures

- Options

- These are contracts that have an underlying asset. The underlying asset can be a "commodity," such as gold, crude oil, silver, or various agricultural products. Alternatively, it can be a "financial product," such as common stocks, bonds, exchange rates, interest rates, stock market indices, or other financial indices.

- Requires less capital, with a high potential for return. Investors place only 10-15% of the contract value as margin. The resulting return (either profit or loss) is therefore a very high proportion compared to the initial investment.

- Contracts have a limited lifespan. For example, they can be 1, 3, or 6 months long. Once a contract expires, the agreement or the rights of the buyer also expire. Therefore, investors must take this feature into account before making an investment decision.

- A derivatives contract has no value on its own. Its value is based on the price of the underlying asset.

- A futures contract has a limited lifespan, whereas a stock investor's ownership has no expiration.

- A futures contract requires a smaller initial investment than stocks. This is because a futures contract only requires a small amount of initial margin, while a stock account must be paid in full for the value of the stocks traded.

- With a futures contract, profits and losses are recognized throughout the trading session. At the end of each trading day, a process called Mark-to-Market takes place, which calculates the difference between the opening contract price and the closing market price of the underlying asset for that day.

The Thailand Futures Exchange Plc. (TFEX) serves as a hub for trading derivatives based on various equities, debt instruments, and commodities, including agricultural products. Under the Derivatives Act B.E. 2546 (2003), TFEX is authorized to arrange the trading of Futures, Options, and Options on Futures of the following types of underlying assets:

- Based on Equities: Securities indices, stocks

- Based on Debt Instruments: Government bonds, interest rates

- Based on Commodities: Precious metals, base metals, energy, agricultural products

- Based on Other Prices and Indices: Exchange rates, carbon credits, commodity indices

There are two main types of margin that investors should be aware of before trading: Initial Margin and Maintenance Margin. When trading derivatives, investors must first deposit an initial margin at a level set by the derivatives broker before trading. After a trade is executed, the broker calculates the daily profit or loss for the investor, causing the cash in the investor's account to fluctuate—either increasing or decreasing—based on the daily price changes of the futures.

The margin rates that brokers charge investors are based on the guidelines set by the Futures Industry Club (FI Club) in the "Standards of Futures Business Operations" regarding margin. Currently, the rates are set at 1.75 times and 1.35 times the rate determined by the Thailand Clearing House (TCH) for retail and institutional investors, respectively.

Initial Margin, also known as a "margin deposit," is the initial amount of collateral that a clearing house or broker requires a futures investor to place. This deposit serves as a guarantee that both the buyer and seller will fulfill their contractual obligations. To open a position, both the buyer and seller must have a balance in their derivatives account that is greater than the required rate. Margin is categorized into three types:

- Initial Margin (IM), also known as a "margin deposit," is the amount of money that both buyers and sellers must have in their derivatives account with a broker before they can open a position. The margin deposit must be greater than the required rate to initiate a trade. The specific amount of the initial margin varies for each product and is determined by the futures exchange.

- Maintenance Margin (MM) is the minimum level of collateral that an investor must maintain in their account. If the balance in the margin account falls below this level (which is 70% of the IM), the broker will issue a “margin call” requiring the investor to deposit additional funds. The investor must then top up the account to restore the balance to the original Initial Margin (IM) level.

- Force Margin (FM), also known as the close-out margin, is the lowest level of margin (30% of IM). If an investor fails to deposit additional margin within the time frame set by the company, they will be subject to a "Force Margin." This means their open positions will be compulsorily closed to ensure the remaining margin does not fall below the FM level.

Investors can place their own trading orders through various programs certified by the Thailand Futures Exchange (TFEX) and service providers, such as Settrade Streaming or MT4. They can also contact an investment advisor for consultation and to place orders for TFEX products. When placing a trade, it's not common to use the terms "buy" or "sell." Instead, the terms "Long" and "Short" are used.

- A Long Position is a buyer's position or a contract stating that the holder will buy the underlying asset at a specified price and time, which is different from buying the asset immediately. Example: If an investor anticipates that the price of the SET50 Index will rise in the next month, they will choose to open a Long Position. If the price moves up as the investor predicted, they will profit from the price difference. However, if the price drops instead, going against their forecast, the investor will incur a loss.

- A Short Position is a seller's position or a contract stating that the holder will sell the underlying asset at a specified price and time, which is different from selling the asset immediately. Example: If an investor anticipates that the price of gold will fall in the next month, they will choose to open a Short Position. If the price moves down as the investor expected, they will profit from the price difference. However, if the price rises against their forecast, the investor will incur a loss.

A Futures Contract is a standardized agreement between a buyer and a seller to trade an underlying asset at a fixed price determined today, with delivery and payment occurring at a specified date in the future. These contracts are tradable on an exchange like TFEX, meaning parties can often offset or transfer their position before expiration. However, if held until maturity, both the buyer and seller are obligated to complete the trade as agreed upon in the contract.

Establishing a Futures Position: You can initiate a position in the futures market by either buying first (going long) or selling first (going short), depending on whether you anticipate the price will rise or fall.

- The buyer of a futures contract is said to hold a Long Position (or simply, to be Long).

- The seller of a futures contract is said to hold a Short Position (or simply, to be Short).

For example,

- on January 1st (the start date), Mr. A enters into a contract by establishing a Long Position (Buy Futures), while Mr. B enters into a contract by establishing a Short Position (Sell Futures). Both A and B agree upon the specific terms of the transaction: the "Underlying Asset," the "Price," the "Quantity," and the "Expiration Date" of the contract.

- On January 31st (Expiration Date), Mr. A purchases the underlying asset from the counterparty at the agreed-upon price, and Mr. B sells the underlying asset to the counterparty at the pre-agreed price. Both A and B fulfill the terms of the contract they committed to.

An Options Contract is a right (not an obligation) to buy or sell an underlying asset at a predetermined price and quantity by a specific date. The agreement is made between a Buyer (Long) and a Seller (Short), and all contract terms (asset type, quantity, price, and expiry) are standardized by the exchange, such as the TFEX. Options primarily come in two types: Call Options and Put Options.

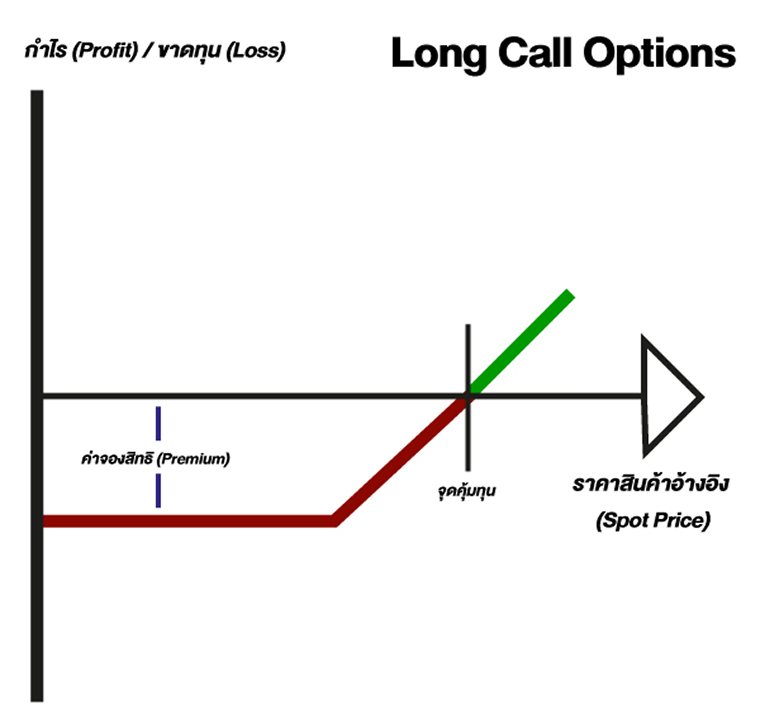

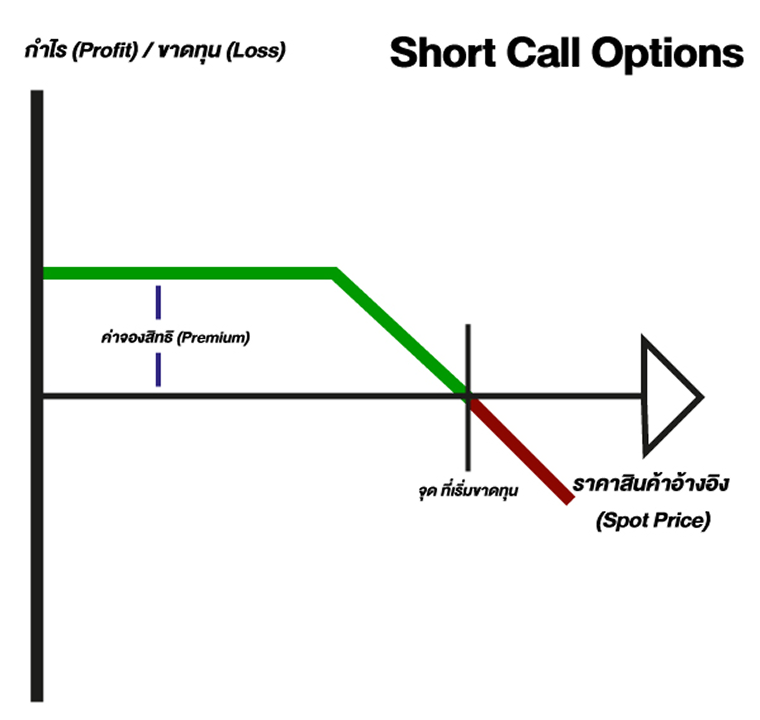

- A Call Option grants the holder (Long) the right, but not the obligation, to buy the underlying asset at the specified price and quantity. The Long party holds the sole discretion on whether or not to exercise this right.

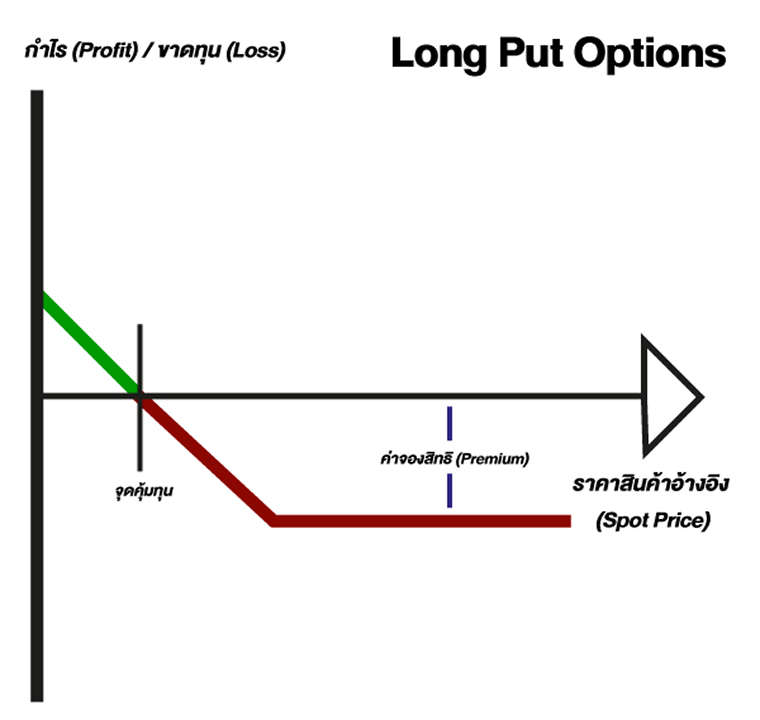

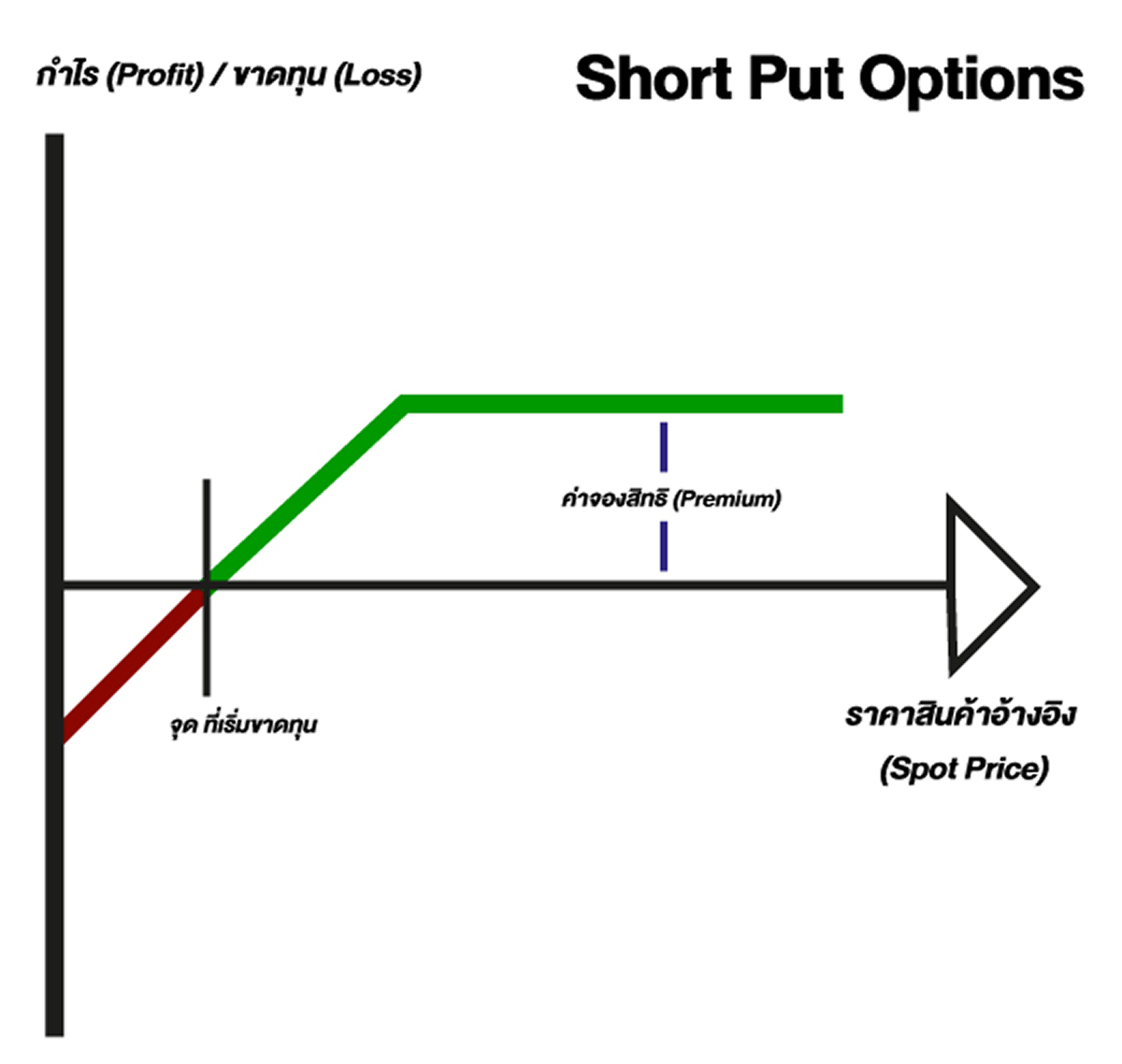

- A Put Option grants the holder (Long) the right, but not the obligation, to sell the underlying asset at the specified price and quantity. The Long party holds the sole discretion on whether or not to exercise this right.

Essential Metrics for P&L Calculation

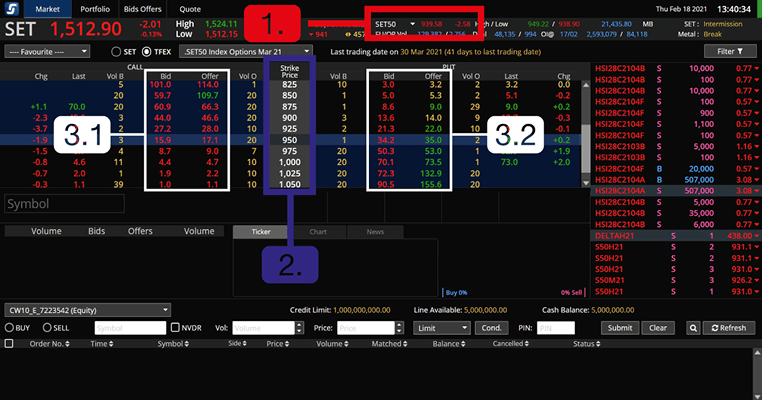

- Underlying Asset Price (Spot Price) (in this case, the SET50 Index)

- Strike Price (also known as Exercise Price): The predetermined price at which the underlying asset can be bought or sold if the option is exercised. Each consecutive Strike Price is set with an interval of 25 points.

- The price of the option (known as the Premium)

- Call Premium

- Put Premium

The Thailand Futures Exchange (TFEX) market consists of both Buyers (Long) and Sellers (Short).

- Buyers of options (both Long Call and Long Put) are only required to pay the Premium (the cost of the right).

If a contract expires "In-The-Money" (profitable) on the final trading day, the option will be automatically exercised and settled via a cash payment of the net profit amount.

If the contract expires "Out-of-The-Money" (unprofitable) on the final trading day, there will be no exercise of the option. The buyer's total loss is limited solely to the Premium that was originally paid. - ผู้ขาย Call (Short Call) และ ผู้ขาย Put (Short Put) จะได้รับค่าเพียงแค่ค่า Premium เท่านั้น

กรณีที่ 1 เมื่อถึงวันซื้อขายวันสุดท้าย “ไม่มี” ผู้ซื้อ (Long) ได้กำไร ผู้ขาย (Short) จะได้กำไรจากค่า Premium

กรณีที่ 2 เมื่อถึงวันซื้อขายวันสุดท้าย “มี” ผู้ซื้อ (Long) ได้กำไร ผู้ขาย (Short) ต้องชำระราคาเป็นเงินสดให้กับ ผู้ซื้อ (Long) ตามจำนวนใช้สิทธิ

Two Methods for Realizing Options Profit/Loss (P&L) Understanding these calculation methods is crucial for forecasting future P&L and managing risk. For example, if an investor holds a Long Call that expires in one month, knowing the current P&L allows them to make a timely decision: Hold the position, take profits, or cut losses before expiration.

- Calculating Profit/Loss from Exercising Call and Put Options (Held to Expiration)

- Long Call Options: Maximum Loss is limited to the Premium paid.

[(Spot Price - Strike Price) - Premium] x 200 = Profit/Loss

*** If the resulting value is less than 0, the investor will incur a loss equal to the Premium."**

- Short Call Options: Maximum Profit is limited to the Premium received.

[(Spot Price - Strike Price) - Premium] x 200 = Profit/Loss *** If the value calculated is less than 0, this represents the number of points lost. This value must then be multiplied by 200 (the Index Multiplier) to determine the final cash loss amount.

- Long Put Options: Maximum loss is limited to the Premium paid.

[(Strike Price - Spot) - Premium] x 200 = Profit/Loss

*** If the resulting value is less than 0, the investor will incur a loss equal to the Premium."**

- The maximum profit for a Short Put is limited to the premium received.

[(Strike Price - Spot) - Premium] x 200 = Profit/Loss

*** If the calculated value is less than 0, this represents the number of points lost. This value must then be multiplied by 200 (the Index Multiplier) to determine the final cash loss amount.

- Calculating Profit/Loss from Exercising Call and Put Options (Held to Expiration)

- Long Call, Put Options => (Current Premium - Initial Premium Cost) x 200 = Profit/Loss

- Short Call, Put Options => (Initial Premium - Current Premium Cost) x 200 = Profit/Loss